SPACs and their consequences

SPACs and their consequences

A surge in public companies and the potential for private market returns in public markets

I wrote previously about the rise of SPACs and thought I would do a follow up with some of the consequences of the explosion in SPACs.

The tl;dr is I believe we’ll see many more companies going public over the next few years. The companies that are “ready to IPO” will still go down that route rather than going public via a SPAC (with some exceptions for notable SPACs). However, SPACs will take companies that are earlier in their life cycle public which will present the opportunity for private market returns in the public markets but there will be a lot of lemons in the bunch.

More public companies

2020 was a record-breaking year for SPACs, surpassing the 2019 numbers by ~5X. There were 248 SPACs raised in 2020, for a total of $83.2B raised. These figures are staggering.

There are currently 225 SPACs currently looking for an acquisition target, and they have 12-24 months to find one.

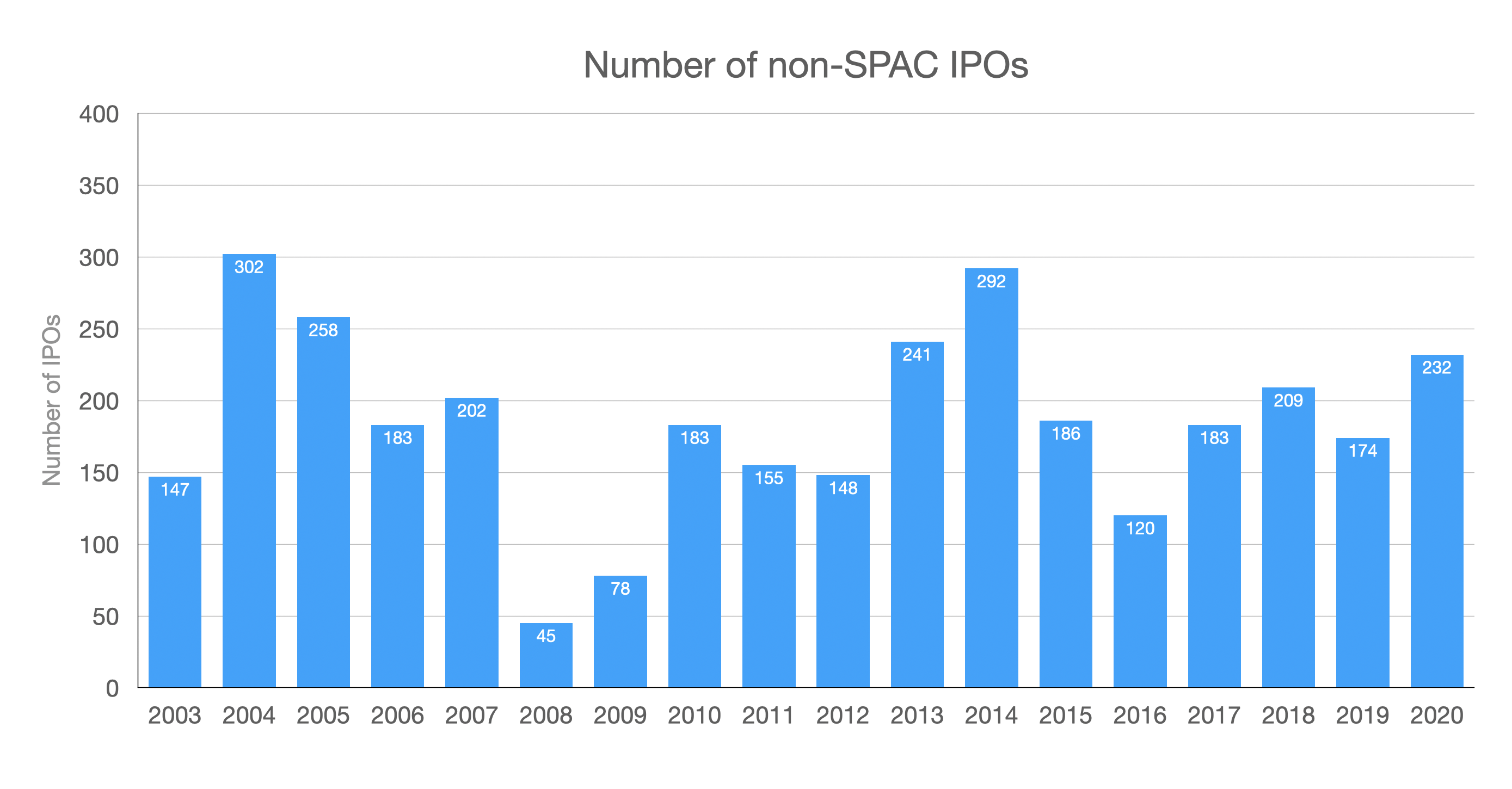

Looking at the number of IPOs (excluding SPACs), we see that in a typical year 150-200 companies go public.

So that means that there are as many SPACs looking for companies to take public over the next 12-18 months as there are companies that go public in a typical year.

So what’s going to happen?

The first question is are most companies that would typically IPO choose to SPAC instead?

I believe the answer is no. Even aside from a lot of the biotech companies which will continue IPOing as usual (which may be out of the universe of companies that most SPACs anyway), I believe most “IPO-ready” companies will choose to IPO/Direct List even despite SPAC interest (minus a few exceptions for extremely notable SPACs - e.g., Chamath’s vehicles, Pershing Square).

The main reason for this is that while the stigma of SPACs has reduced over the last few years, I expect the stigma to re-appear over time. Even now, based on discussions with friends who are bankers or employees at pre-IPO companies, there seems to be a belief that the SPAC should only be seriously considered if the price is unbelievable or if the company isn’t “IPO-ready”.

So if most of the companies that go public through traditional means will still go public through traditional means, what’s going to happen given the hundreds of SPACs seeking companies?

While some may not be able to close a deal, I believe most of them will tend to find a company to take public, which should lead to an increase in the number of companies going public each year over the next few years.

Deal Completion and Adverse Selection

So why will most of the SPACs find a company to take public? Because i) they’re highly incentivized to do so and ii) there are enough companies out there.

A SPAC sponsor typically has two years to complete a transaction and typically gets 20% of the size of the SPAC in equity along with additional warrants. If a transaction doesn’t take place, then the money the SPAC raised is returned to investors.

Given the above, a sponsor is highly incentivized to complete a transaction. And while the transaction needs to be voted on which provides for some form of checks-and-balance, overall it’s not unreasonable to think that as a SPAC gets closer to that 2-year deadline, one may drop the quality bar somewhat because taking something public is better than taking nothing public and liquidating the SPAC. This may lead to adverse selection and keep investors away from some SPACs.

Also, it is evident that the public markets, in this low-interest rate but capital abundant environment are thirsty for growth assets, and the universe of private companies is large, and so most SPACs should be able to find a company (which likely might not be ready to IPO itself in terms of performance) to take public via an acquisition.

Per McKinsey, post-2015, more than 90 percent of recent SPACs have successfully consummated mergers, whereas, before 2015, the number was below 80%. I expect the numbers to drop somewhat given the massive increase in the number of SPACs, but still expect 80-90% of these SPACs to find a company.

Note that this potential for adverse selection, especially as a SPAC gets closer to its 2-year mark, is one of the reasons I believe that the stigma around SPACs will continue to linger, and why many of the companies that have a history of strong performance and can IPO/Direct List will choose to go that route.

It’s worth considering who the SPAC sponsors are and their track record when investing in a SPAC. The more reputable a manager, the less likely they would risk their track record by taking a bad company public instead of returning the money.

Private Market Returns and Risk

So which are the companies which these SPACs end up taking public then?

The analogy I like to think of is that if today, the companies going public are those at the Series F and beyond stage, SPAC’s will predominantly take the series C and D and E companies public.

What I mean by this is that these companies will be less further along in terms of the milestones they’ve achieved before going public.

While most of the companies that IPO today are unprofitable, they tend to have a path to profitability or a track record of years of revenue and revenue growth.

The companies that SPAC will likely be even further away from profitability, be smaller, and have a lower revenue base generally (and some might even be at zero revenue or pre-product launch). They will essentially be earlier in the life cycle but have the potential for large revenue increases.

Why is this? Primarily, because of the SPAC regulatory arbitrage.

The SPAC Regulatory Arbitrage

Of all the advantages of SPACs, one of the primary ones vis-à-vis IPOs is that SPACs allow for providing future projections of operating performance.

This enables a company or startup which is still early in its trajectory, to clearly outline the potential revenue and cash flows it can be producing 3-5 years from going public if things go well. This articulation makes it easier to tell the story to investors of an earlier stage company that might not have the existing revenue/track record at the time of why they may succeed.

There are other advantages of SPACs in particular that it is faster and has less onerous reporting requirements and so better for these earlier in their lifecycle companies to use to go public.

SPACs and private market returns

Over the last decade or so, companies have been staying private for longer, given the availability of enough capital at attractive valuations reduced the need to go public from a capital perspective. However, what that has meant is that as companies do go public, they are later in the journey and so more of the returns are captured by private market investors relative to public market ones, as the albeit dated chart below shows.

With earlier in the lifecycle companies going public via SPACs, the benefit for retail or public market investors is that there are likely to be more promising companies that create value while public. Note that this was the norm previously, with many companies such as Amazon, Microsoft, Apple and Adobe up >500X from their IPO price. But with companies over the last decade or so tending to delay their IPOs and going public at >$10B valuations or even >$50B valuations, the upside for public markets was more limited.

However, given the SPAC incentives highlighted above, and that the companies going public via SPACs are earlier in the journey, there is likely to also be more risky assets and scope for speculation (i.e., investors betting on whether a pre-launch SPAC’ed company actually launches the product they have planned or companies projecting rosier than reality future financials).

Closing Thoughts

There will be many more companies going public in the next few years. Some of the more mature ones will likely choose to go ahead with an IPO or a direct listing, but many earlier stage ones will end up going public via a SPAC.

These companies will present the opportunity for private market like returns (i.e., the 10, 50, 100X returns), but will come with risk and speculation. Some may even go to 0, as is expected by a VC for a proportion of their early-stage companies.

But there will likely be some gems in the pack, that can perhaps deliver returns to public market investors such as an Amazon, Microsoft, Adobe, or Apple (all >500X from IPO).

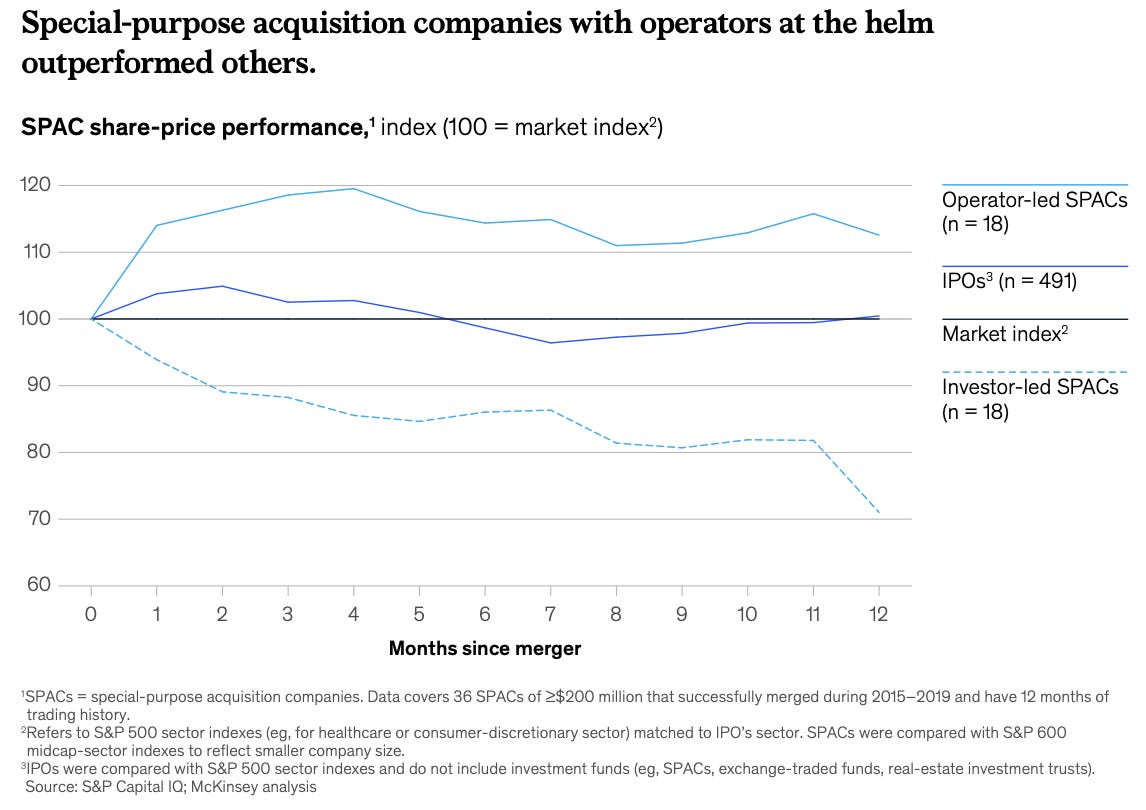

Lastly, it’s worth thinking about who the SPAC Sponsor is, and the expertise they have. While the sample size is small, data shows that focused operator-led SPACs tend to outperform investor-led ones. But more generally, there will likely be a lot of lemons going public via SPACs, and so investors should consider which sponsor they’re willing to invest alongside.

Thanks for reading and wishing you a very happy new year! If you liked this post, give it a heart up above to help others find it or share it with your friends.

If you have any comments or thoughts, feel free to tweet at me.

If you’re not a subscriber, you can subscribe below. I generally post once a week or every other week on Monday about things related to technology or business.