The Long-termism of the Stock Market

There’s a belief that the stock markets take a very short-term perspective. While there are some valid arguments for this particularly around the pressures of quarterly earnings which I touch on later in the piece, I believe markets take a fairly long-term horizon, which can be seen in the prices reflected in the market historically.

What Prices say about Time Horizons

The market’s P/E ratio

The easiest way to think about this is to consider the S&P index in its aggregate.

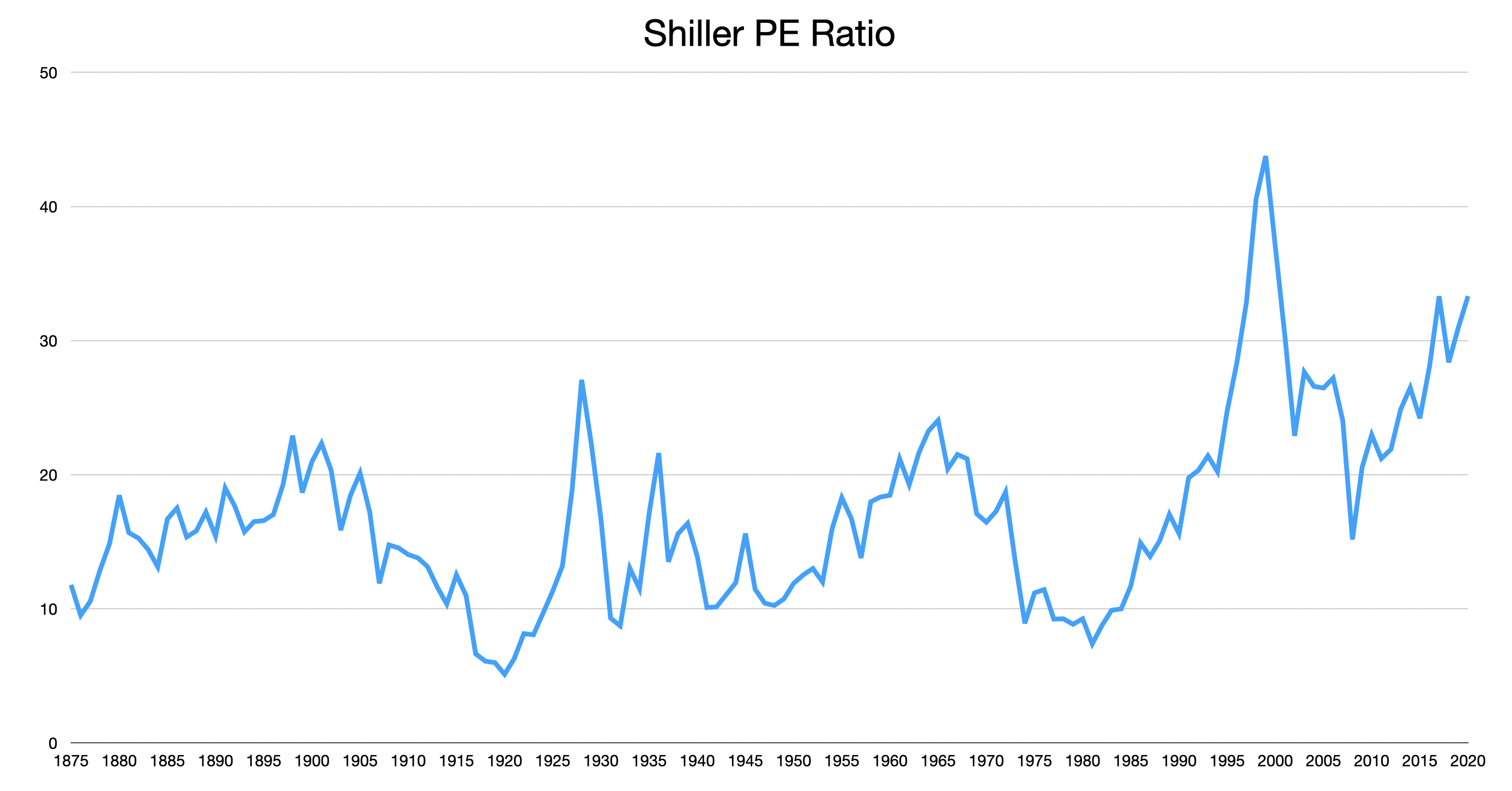

Using the Shiller PE ratio graphed below which is the ratio of the aggregate price of the index to aggregated inflation-adjusted earnings, one can see that the index has been priced at typically 15-25X of companies’ average earnings for their stock.

Investors get paid back using cash flows and to the extent that they’re pretty close to the earnings for the index in the aggregate, the market’s valuation suggests it is looking into the future approximately 15 years when valuing the company.

In other words, if markets were short term, it might only place an emphasis on what companies make in the immediate 3-5 years which would lead to companies being valued closer to 5X earnings.

Dividends and Cash Flows

A more precise way to think about it is as follows. Companies are valued on the basis of the present value of their free cash flows. In a short-term market, stocks would be valued largely based on cash flows or dividends in the immediate years, because markets wouldn’t care much about the cash flows beyond say 5 or 10 years

But is that reflected in the actual valuations?

From a 1992 paper, only about about 10-15% of the stock price of the Dow Jones Industrial companies comes from expected dividends over the next five years.

That means that the lions share of a companies equity value placed on it by the market, is coming from the long-term dividends paid out in year 6 and onwards.

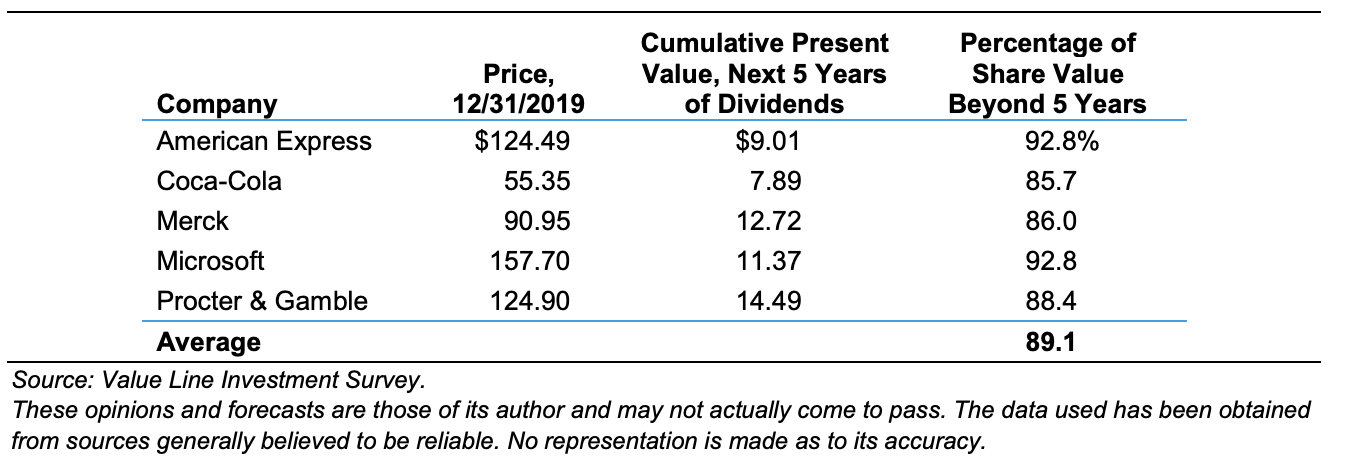

A more illustrative example is below, via Michael Mauboussin. As seen below, for each of five large stocks, over 85% of their value is coming from expectations of dividend beyond 5 years. Would a short-term market think like this?

The SaaS industry example

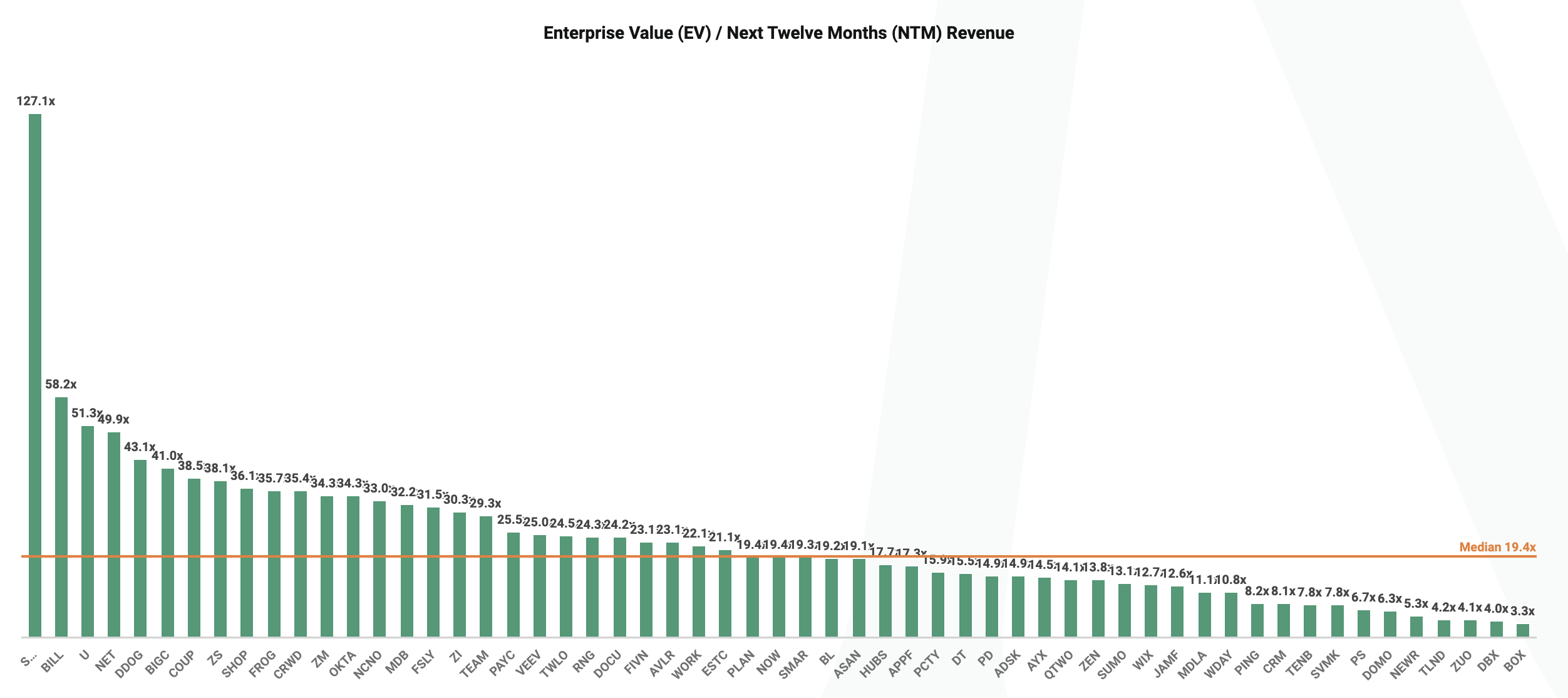

I think looking at the entire SaaS industry is a good example. That any company let alone pretty much the entire industry can be “valued on” revenue multiples rather than free cash flow multiples is a sign that markets are long-term thinking.

The fact that the entire industry is valued at 20X revenue (let alone individual companies being value at over 40X revenue) shows that the markets are capable of thinking very long-term about the potential earnings power of these companies, and able to bake it into their valuations.

If you consider that most SaaS companies aren’t generating profits or free cash flow or have ever paid dividends, 90-95%+ of their stock’s value is coming from free cash flows more than 5 or even 10 years in the future.

The Short-Termism Argument

The typical argument against the long-termism of markets is the pressure to hit quarterly results which leads to companies operating on a “90 day clock”, rather than being able to invest for the long-term. It’s worth unpacking that a bit.

“We’re no longer beholden to the expectations of shareholders, or as I like to call it, the 90-day shot clock” - Michael Dell on running Dell as a private company

Quarterly Results

Yes, companies have to report quarterly results, and there can be a pressure to hit them. And yes, companies stock prices can drop, sometimes by a lot, if they have a poor quarterly earnings report.

Does that mean markets are short-term? Consider the following:

Guidance and Expectations: Companies set their own guidance, and analyst forecast and expectations tend to be centered around those (and other conversations and data points from management). While there is pressure to meet guidance and expectations, companies investing in the long-term can adjust future guidance accordingly.

Narratives matter: While lower guidances by themselves can be seen as a sign of weakness, if companies are able to clearly articulate a story to shareholders, they can be more than willing to support short term losses or reduced profits for investments in the long term.

Large corrections are sometimes justified: Because stocks are valued based on the present value of long-term cash flows, sometimes even a small miss in quarterly results, whether it be on the top line or bottom line might actually necessitate a large decline in the stock price. Not because of the miss itself, but because what the miss might imply of the long-term future cash flows of the business. For example, a miss could suggest that a moat isn’t as strong as believed to be, or a companies long-term penetration of its TAM is likely to be lower than believed, which has often large implications for future cash flows, and correspondingly on stock prices.

Fluctuations are common

Another related part to the argument above is that stock prices can move a lot, and often without reason. If the market was truly long-term, this wouldn’t happen too much, because day to day events don’t change a companies value like that.

This is one of the realities of the market where some fluctuations are common. Stocks respond to day-to-day macroeconomic news and movement. But even more so, while the stock price is based on the long-term value of the company, in the short term these stock prices move based on the supply and demand of the stocks.

In some sense, people are making (sometimes) short term bets on the long-term performance of the company, which leads to these fluctuations.

As Ben Graham famously said:

“In the short run, the market is a voting machine but in the long run, it is a weighing machine.”

The fluctuations and price movements in the short term are usually noise, but in the long term, the performance and cash flow potential of a business gets reflected in their share price.

Managerial Incentives

Another closely related idea to the short-termism of the markets is that of managerial incentives and the time-horizon managers take, arguably from pressure from the markets.

With CEO tenures on the decline, and with contracts tied to incentive measures, CEOs (and management overall) may feel the need to hit short-term performances. Measures such as earnings per share in particular are not great for this, since those can be “managed” by reducing investments in long-term projects or other means.

CEOs may also be incentivized to focus on the short-term duration during which they are in charge, and disregard the long-term consequences of their decisions if they don’t think they’ll be in charge to face the repercussions.

These are absolutely true and one of the issues stemming from the agency in markets . Unfortunately, the markets don’t have complete information about the inner workings of a company, and are forced to extrapolate from performance reported every few months. In the absence of additional information, a CEO focused on driving short term earnings / performance may be rewarded in stock price increases because the market may view that as a sign of future strength. But only until they realize it came at the cost of long-term.

Another way to think of it is this. Because many CEOs act short-term due to incentive structures, the market may also be forced to take a shorter-term outlook on companies. But CEOs who have right incentive structures in place and the trust of their boards and want to invest in the long-term can guide the market to taking that longer-term horizon towards their company too.

The Amazon Example

Perhaps the best example of the ability of markets to be long-term is Amazon and Jeff Bezos.

Amazon was rewarded with patience and the capital from shareholders to take big and bold bets (which occasionally failed) and invest in the long-term while still being valued richly rather than on the basis of their earnings (which were artificially low given the investments in growth).

Bezos did not need supermajority control of Amazon to take a long-term orientation. He simply was able to educate the shareholders on Amazon’s plans, and gain their trust, which allowed Amazon to invest in the long-term while being a public company. Two things stand out in that regard: the importance of controlling the narrative and ignoring the fluctuations which will still arise.

Controlling the Narrative

As I touched on last time, Bezos from the outset outlined the principles and philosophy Amazon would follow when evaluating its success.

“We will continue to make investment decisions in light of long-term market leadership considerations rather than short-term profitability considerations or short-term Wall Street reactions.”

He also highlighted the focus on cash flows rather than earnings, given the investments in the long-term

“When forced to choose between optimizing the appearance of our GAAP accounting and maximizing the present value of future cash flows, we’ll take the cash flows.”

Ignoring Short-term Price Movements

Even in the case of Amazon, the stock saw large fluctuations which went against the direction the business was moving in. In 2000, their stock was down 70% compared to 1999 after the tech bubble euphoria ended.

Bezos referenced the Ben Graham quote from earlier in this piece, and also wrote the following:

So, if the company is better positioned today than it was a year ago, why is the stock price so much lower than it was a year ago? As the famed investor Benjamin Graham said, “In the short term, the stock market is a voting machine; in the long term, it’s a weighing machine.” Clearly there was a lot of voting going on in the boom year of ’99—and much less weighing. We’re a company that wants to be weighed, and over time, we will be—over the long term, all companies are. In the meantime, we have our heads down working to build a heavier and heavier company.

Further Reading

Here are a couple of good reads on this topic if you would like to go deeper!

Mauboussin and Calahan’s A Long Look at Short-Termism

Thanks for reading! If you liked this post, give it a heart up above to help others find it or share it with your friends.

If you have any comments or thoughts, feel free to tweet at me.

If you’re not a subscriber, you can subscribe below. I generally post once a week or every other week on Monday about things related to technology or business.