Startups and TAMs

Startups and TAMs

Why TAMs don't matter but thinking through TAMs can be helpful

Hi friends!

I didn’t think I’d be writing about Total Addressable Markets but here we are. Every startup pitch deck (or company S-1) has a slide or section about TAMs. But in the quest to show large TAMs to entice investors, sometimes the TAM number has become meaningless. That’s what I’ll be discussing today.

I’ll cover:

TAMs, SAMs, and SOMs

Do TAMs matter for Startups

How TAMs are helpful

How to calculate TAMs

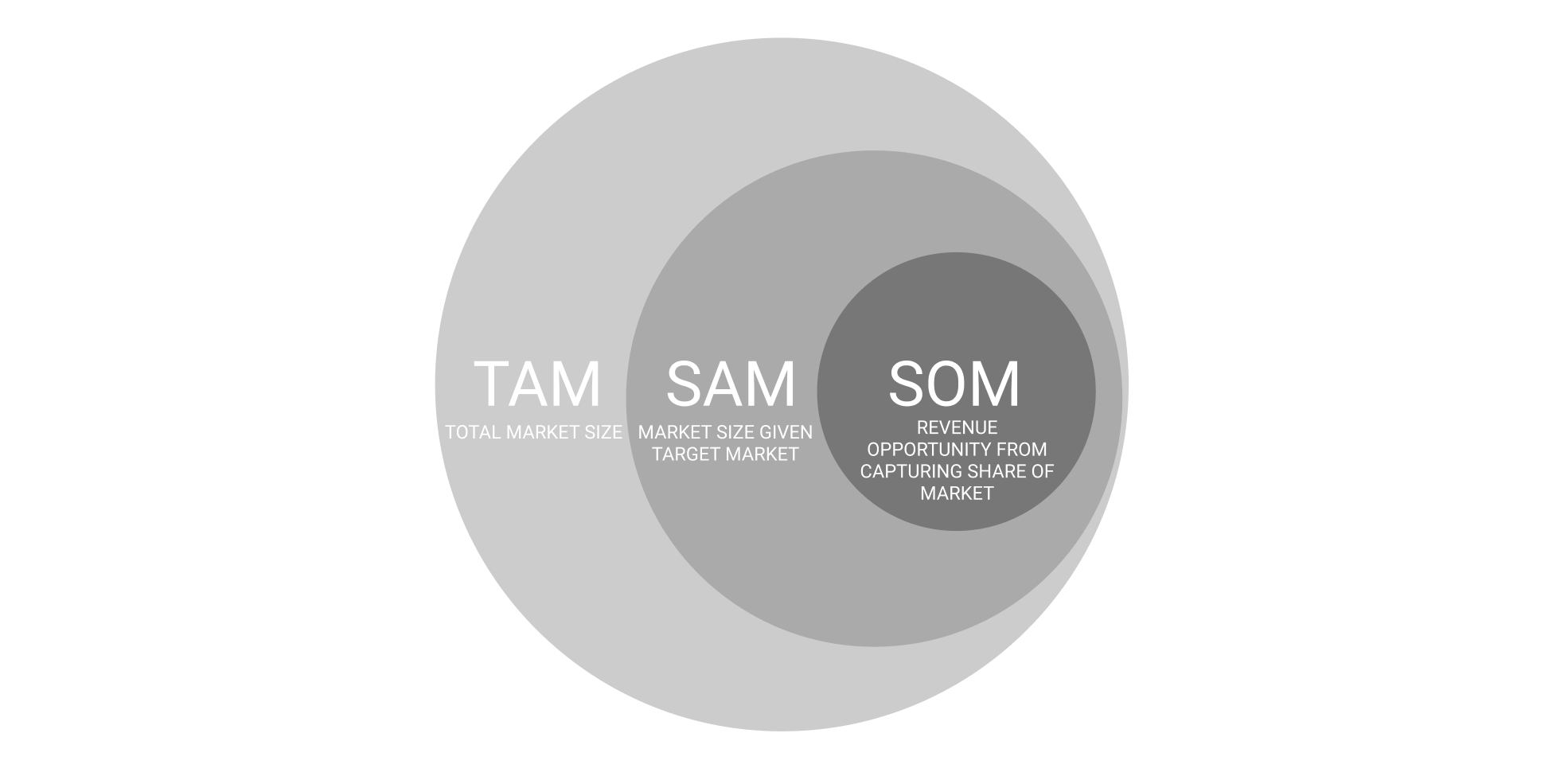

TAMs, SAMs, and SOMs

TAM stands for Total Addressable Market and refers to the maximum theoretical revenue potential of a company at that moment given the products or services it has.

Strictly speaking, when considering the Total Addressable Market for a company, we ignore the realities of the company (its target segment of customers, its geographic boundaries, etc) and just consider, given its products or services how big is the (typically global) market for that product or service.

To add a bit of realism to these numbers, SAMs and SOMs are helpful.

SAM, which refers to the Serviceable Addressable Market, represents the realistic revenue opportunity for the company given the current:

target market / customers

geography

specific SKUs / products

It is a subset of the TAM, and evolves both as the market evolves and as the company expands GTM motions and geographies.

So TAM is the suspend disbelief market size and SAM is the realistic market size. But no company captures 100% of its market, and so that is where SOM comes in.

SOM is the realistic revenue opportunity for the company given it captures some share of its SAM, The realistic share will depend on things like industry structure and market dynamics of the market and how fragmented the market tends to be.

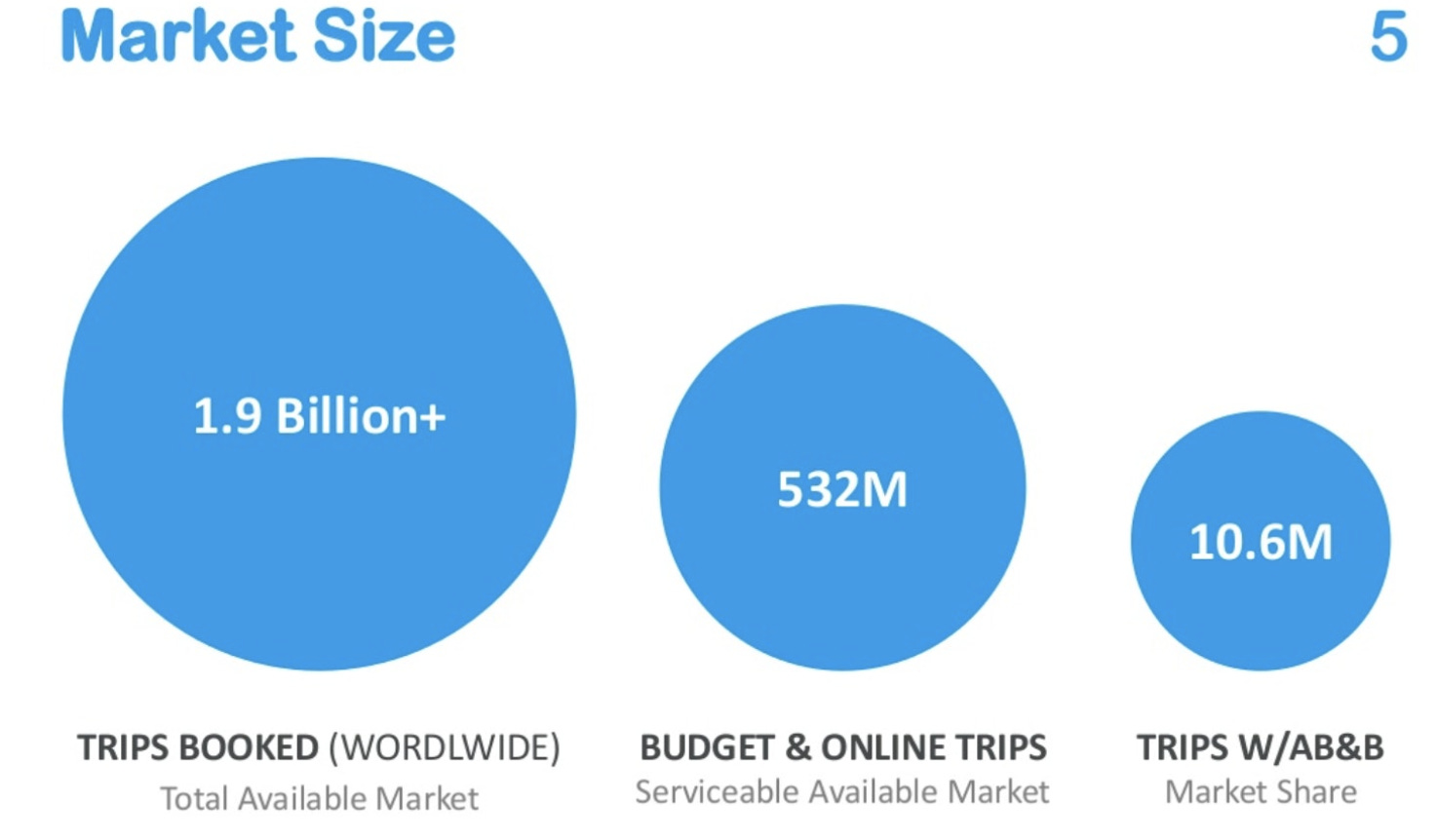

Here’s an illustration of it from Airbnb:

Do TAMs Matter for Startups

Generally, at the early stages, there tend to be two kinds of startups:

those going after nonexistent or very small but very fast-growing markets or new categories

those going after established markets or industries

1. New markets

In the first case, TAMs rarely matter because the market is evolving so rapidly. Besides, a product that is a meaningful improvement can itself 10x the TAM.

Consider NFTs: the TAM for “digital art” or “digital collectibles” a few years ago as people were starting to build elements of the NFT value chain was essentially nonexistent. But the right companies (Topshot, Sorare, Opensea), helped unlock and grow that market.

In some cases, one part of the TAM exercise that is useful in thinking about whether there is a similar behavior that something that your product or service might take share from, and what the TAM of that broader market might be. So, in this NFT example, you could consider the TAM as art or collectibles. That would help show that the size was massive, although the behavior didn’t currently exist, and so the SAM and SOM today were very small. But the right tools along with changes in behavior could help “digital” capture some of that TAM of the broader market.

This is only applicable in some cases though. Consider the Operating System market before Microsoft. That exercise would be a lot more difficult, especially at that time, and not with the benefit of hindsight.

Peter Fenton touches on why the thinking that you need big TAMs isn’t true:

“It’s the markets that don’t exist that you create. Like, what was the search market before Google? What was the operating system market before Microsoft? What was the cloud business before Amazon? The thinking of big TAM is so myopic.”

2. Existing or Established Markets

In the case of startups going after existing industries or problems, TAMs matter more since in some cases they put a ceiling on the size of the opportunity, but great companies that improve the experience can still grow the TAM.

Let’s consider one case where TAM’s might be difficult to change, even with a lot better product. Say for example a healthcare startup is building a product to better manage or cure a specific disease. The TAM here is very relevant because whether 1,000 people get the disease in the world or 1M (and the corresponding amounts that can be charged) make a big difference. No matter how good your cure is, the market for this disease is limited. TAM expansion is an option, where the company can go after adjacent areas, but may not be simple. These are cases more than most where TAMs matter.

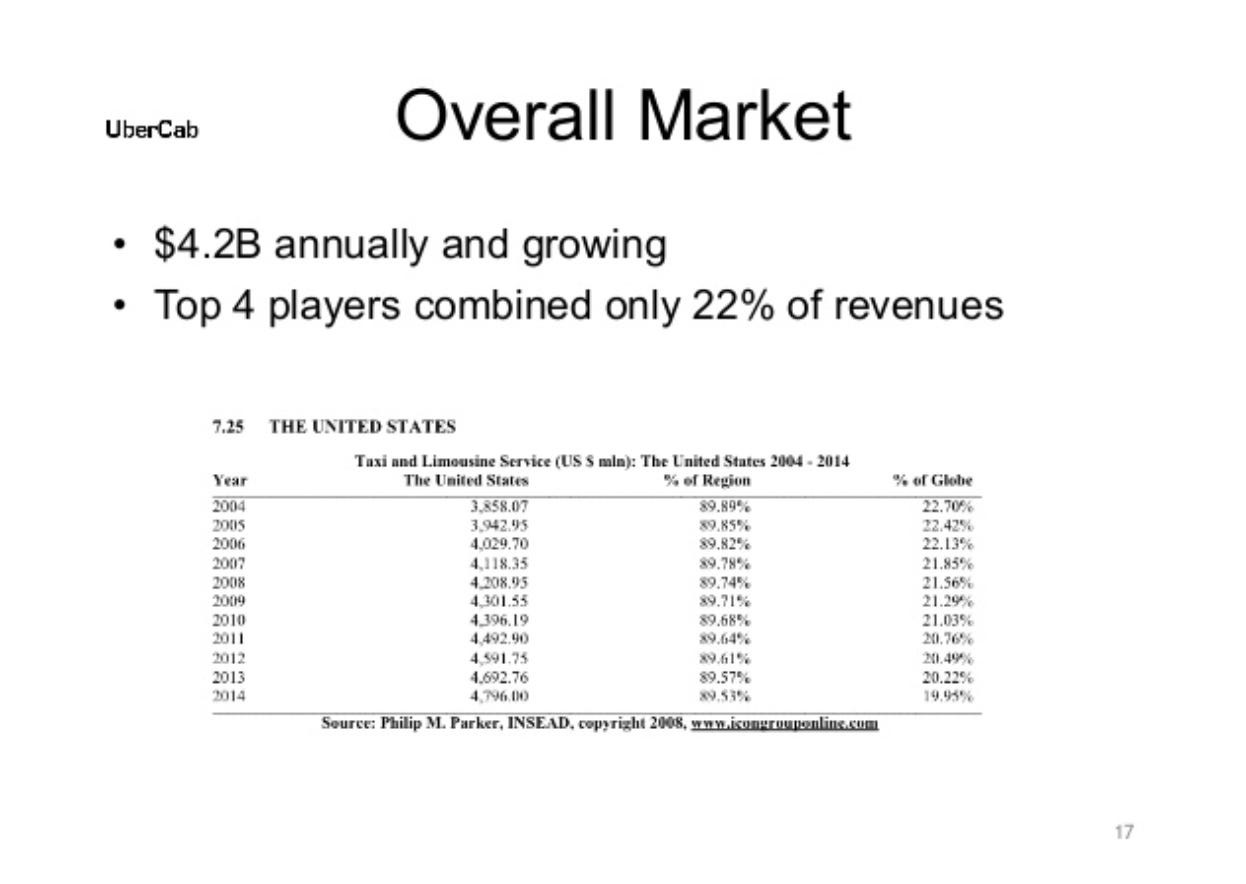

Let’s consider another case of an established industry: Uber and Taxi's/Limousines. From Uber’s Seed pitch deck, the size of the overall taxi market was $4.2B.

In 2019, Uber by itself did ~$65B of bookings. Talk about expanding the TAM.

Yes, there was category expansion (Uber Eats), and geographic expansion (serving other countries), but even just in the US Uber did ~$25B in mobility bookings in the US, larger than the entire taxi and limo market when they pitched their seed. So they were able to grow the market itself,

How TAMs are helpful

So, we just concluded that TAMs don’t matter too much for startups. But why then should we bother with them? The obvious answer is that some investors still care and want to see them in pitch decks, but here are some reasons why I believe it’s helpful:

Occasionally, prevents going after a certain opportunity: This is rare, but sometimes founders will realize through a TAM exercise that the opportunity is not worth going after, saving themselves a lot of time.

Forces thinking about market structure and dynamics: Simply going through the exercise of thinking through TAM forces founders to think about i) whether this is a new market or an existing market and ii) consequently distribution strategy. One proxy I heard on a podcast that I, unfortunately, can’t place anymore but liked was “are customers currently searching for something like your solution? If you could rank #1 on Google search for one search term what would you choose?”

Encourages thinking about TAM expansion: If the current TAM is small, doing the exercise encourages founders to have a plan for how that TAM expands over time. Thinking through that on day 1 is helpful because it may influence how the company is architected. Some ways that TAMs grow:

Natural growth in TAM of the market due to industry and market forces (thinking audio, NFTs, or remote work software today)

Growth in the market because of a vastly superior product experience (i.e., Uber growing the taxi market)

Expansion of company’s TAM through geographic expansion (Uber expanding countries or cities)

Expansion of company’s TAM through category expansion (Uber adding Eats or freight)

Encourages thinking about a business equation/value creation formula: When calculated in a bottom-up manner, TAMs often encourage thinking through the key equation of the business of how value gets created, and the main levers that drive the revenue of the business.

Calculating TAMs

The above benefits of thinking through TAM are helpful if done the right way. Before I go into what I believe is the right way, here are some pitfalls I occasionally see in decks:

Ignoring the nature of your product or service in the TAM: Sometimes a startup takes a very broad view of the industry they operate in which isn’t tied to how they make money in that industry. For example, a construction or healthcare software startup stating that the market size for healthcare or construction is $XT. Sure, that’s right, but that’s not the market size for the software part of it.

Using arbitrary numbers to go from TAM to SOM or SAM: The use of broad assumptions around what percent of the whole market can be captured, that isn’t supported by anything. For example, a startup that sells HR software saying, the HR software market is $XB and we can capture 30% of it so our SOM is 0.3X. Do you cater to the whole market? Where does the 30% come from? Would you be the #1 player in that market? Does Salesforce have 30% of the CRM market?

In general, I think the above pitfalls are driven by trying to calculate TAM in a top-down manner rather than a bottom-up manner and/or not going from TAM fully to revenue opportunity.

To go into that, let’s look at the three ways to calculate TAM: top-down, bottom-up, and value theory.

I’ll use one example throughout to help illustrate: say the product which helps brands find podcasts to advertise on (i.e., connect brands to podcasters).

Top-down approach

This typically involves the use of broad-based market research-type reports which show how big the industry is. It’s very important to hone in on the parts of the problem that one is attacking when using this or it has the potential to be wildly off or just a meaningless number.

So in the example above, a top-down approach to TAM might be that Gartner believes the digital ad market is $320B which is the current TAM.

This might be “wrong” in two ways,

doesn’t recognize that the company operates in a subset of that market (audio)

doesn’t recognize that the company won’t capture the entire dollar of advertising spend as revenue given its model.

A more correct way to think about it might be: the current podcasting ad market is $1B. But even this doesn’t consider the second bullet above yet.

To get one level further, we can recognize that we’re a marketplace and will take a 15-20% cut on transactions, so our revenue opportunity is ~$150-200M if we capture the whole market.

Bottoms up approach

This usually involves calculating TAMs by starting with the number of customers that would use something and what they would be willing to pay. I much prefer this approach as it tends to involve thinking through how the company creates value and how big the potential customer base really is and what the willingness to pay is. It’s also more useful when considering new business models or businesses which change how an industry may work.

In the example I used above, one way to think about it might be as follows:

The hours spent listening to podcasts is 15B hours.

At an average ad load of 10%, that would be 1.5B hours of ads.

Ads are an average of 20 seconds, so that would be 270B ad impressions.

At a CPM of $5, that would be $1.35B

And if we take ~20% cut of it, that would be a ~$270M revenue opportunity.

It’s important here to consider the company’s model. For example, if the company intended to charge companies for its product in a SaaS model rather than a marketplace, an alternative way to think about this would be:

10,000 businesses spend money on podcast ads (a more accurate way would be to segment them by size)

We believe the average revenue per business we can generate is ~1000/month

Therefore the TAM is 10,000 * 1000 * 12 = $120M

Note that from TAM to SAM to SOM you have to consider what businesses you’ll serve (may only SMBs?) and what percent you can capture.

The good thing about this approach is that you can play around with the numbers to see how a vastly superior product that say can increase ad loads or increase CPMs by better matching can grow the size of the market. It also shows you’re thinking about the key variables related to the market.

Value theory approach

This works best typically for new products or products in new markets and involves identifying what value they are receiving from the product and how much of that value they would be willing to give up. The pricing obtained from this approach can sometimes build into calculating a bottoms-up TAM.

For the example above, say we believe that our product can increase CPMs by better matching the right brands to advertisers.

One way to articulate that in the TAM is as follows:

At ~$5 CPMs, the size of the market is $1B.

We believe we can grow CPMs to $10 by better matching and dynamic ad insertion

Based on surveys, podcasters are willing to pay 50% of the improvements in CPMs to us.

In this case, what is happening is that for those who become your customer, you capture 50% of the 100% improvement and so TAM is essentially 50% * ($10 - 5)/5 * $1B. = $500M

In this case, you can effectively grow the market by serving customers by making the market more efficient through better brand and podcaster matching, and the TAM reflects that value you provide and the WTP of that value.

Closing Thoughts

In summary, for most startups, TAM (at that moment in time) doesn’t matter too much because:

Many startups operate in new markets where TAM is small initially or even nonexistent

The very best companies grow the markets that they operate in by introducing fundamentally new or superior experiences

Most companies can expand their TAM by either going broader to bring in new customers (e.g., adjacent geographies), serving the customers in more ways (product/category expansion) or taking over more parts of the value chain (so a higher percentage of the gross revenue gets converted to net revenue)

However, calculating TAM’s can be a worthwhile exercise because it forces you to think about the dynamics of the market and the business and how value gets created and captured.

When doing so, I recommend using the bottoms-up or the value theory approaches or at least thinking about how your startup makes money given its business model, and not just using the market size of the broad industry as your TAM.

Further Reading

Bill Gurley’s How to Miss By a Mile: An Alternative Look at Uber’s Potential Market Size

Sleeper Thought’s collection of TAM slides from successful startups

Thanks for reading! If you liked this post, give it a heart up above to help others find it or share it with your friends.

If you have any comments or thoughts, feel free to tweet at me.

If you’re not a subscriber, you can subscribe below. I write about things related to technology and business once a week on Mondays.

Thinking about SOM for my startup also helped me think about the market/industry dynamics.

Is this a winner take all market or can multiple big companies coexist? Very important if your product has some social aspects or other kinds of network effects.