Reasoning Revenue Multiples

Reasoning Revenue Multiples

Understanding what is embedded in the high revenue multiples of today

Scott McNealy, the CEO of Sun Microsystems famously quipped the following after Sun’s stock had run up to $64/share before falling to under $10/share a year later during the dot com bubble.

At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?

In light of that comment, it’s worth considering the case of public high growth SaaS companies today which tend to be valued on revenue multiples with the median one trading at ~25X EV/NTM revenue.

So what are we thinking?

Is it absurd that companies are trading at 20X+ revenue multiples? While it isn’t as simple as McNealy’s comment above might imply, it does provide us a good starting-off point to answer this question.

For one, stocks should be valued as the present value of all future free cash flows (FCF) of a company, since that is what can be returned to investors as dividends. While revenue is obviously a key driver of that, as McNealy alludes to, the bottom line is more important and ultimately free cash flows and not revenue is what matters.

Now, depending on a stage in a companies life cycle, it might be difficult or even impossible to actually project out all its future cash flows, and so revenue multiples are often to triangulate valuations.

But as a company matures, over times its valuation anchors around what it actually generates in earnings and then free cash flow, as Chamath touches on in this tweet below.

Note however that McNealy’s tongue-in-cheek quip misses the importance of revenue growth and secondarily the impact interest rates have in valuations. Something valued a 20X revenue growing at 100% y/y for two years could soon be at 5X revenue in a few years. Similarly, one might be willing to pay 10X revenue when the risk free rates is 1% but not when it is 7%, since the discount rates will be lower.

Embedded Expectations

How do we put all this together? One way to do that is to try to understand what expectations of future performance are embedded in the current stock prices to make sense of what a 20X or even 50X revenue multiple is actually implying.

As mentioned earlier since FCFs are what matters, companies (yes, even SaaS companies) will trade based on FCFs eventually. So let’s say in 10 years, most of these companies will trade based on free cash flows rather than on revenues (the idea one might be willing to wait 10 years might be ludicrous in itself to some people, so one can repeat this exercise with whatever number they are comfortable with).

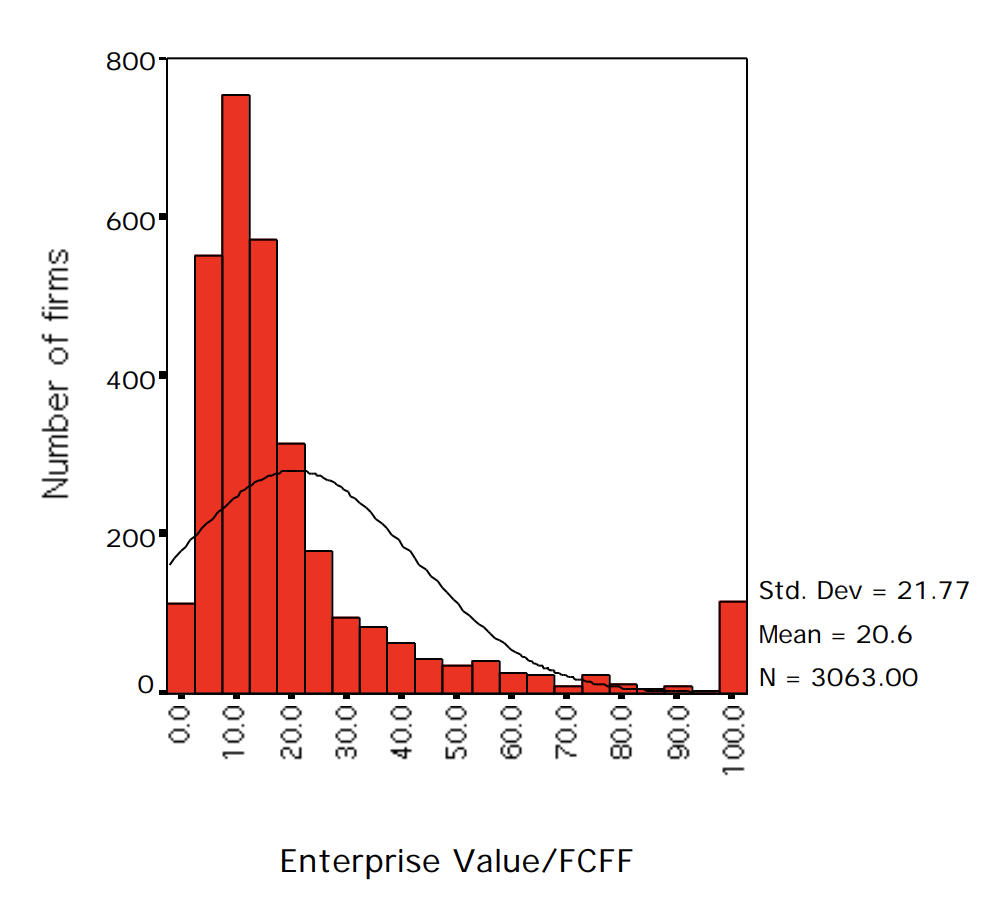

Now, how much free cash flow will they generate then? That will depend on how efficiently they can convert Revenue to FCF, or their FCF margin. Its important to use what we think they’ll do repeatably at scale / maturity, rather than what they’re doing now. This will vary sometimes quite dramatically between companies just given differences in business model, market, gross margins and so on. This is also evident in today’s numbers in the chart below via PublicComps, although most of these businesses are not at maturity and still growing quickly. For most actual SaaS businesses, I anticipate a 30%-40% FCF margin at scale, although their gross margins today might give a hint at whether they’ll be below that range or in the upper end of that.

Lastly, at scale, what multiple of FCF’s should they trade at? That will depend on a lot of things, such as how durable the FCF’s are, how fast FCF’s are growing (less important since we’re assuming some sense of scale / maturity), what the interest rates are at the time, and so on.

From an earlier analysis by NYU professor Aswath Damodaran, the median company typically trade at ~20X FCF. But given lower interest rates translate to higher multiples, and a better business model (recurring revenue) leads to more durable FCFs, I think its fair to say that let’s say that SaaS companies will trade at 30-35x FCF at scale.

So again, these are the key assumptions:

The time period from now companies will be close to scale and trade on FCF multiples

What percentage of their revenue is converted to free cash flow (FCF margin)

What multiple of FCF they will trade at

Now given these assumptions, we can work backward to estimate what expectations are embedded in a companies stock price and in their revenue multiple today.

Specifically, we can estimate what kind of revenue they will need to be at 10 years from now and also what kind of revenue growth CAGR they will need to sustain to get there. Another thing one can do is see what market share of their addressable market the company will have to capture, but I don’t particularly like this one since TAMs change and grow over time as companies enter new spaces and markets change.

What does this mean for Zoom and Snowflake?

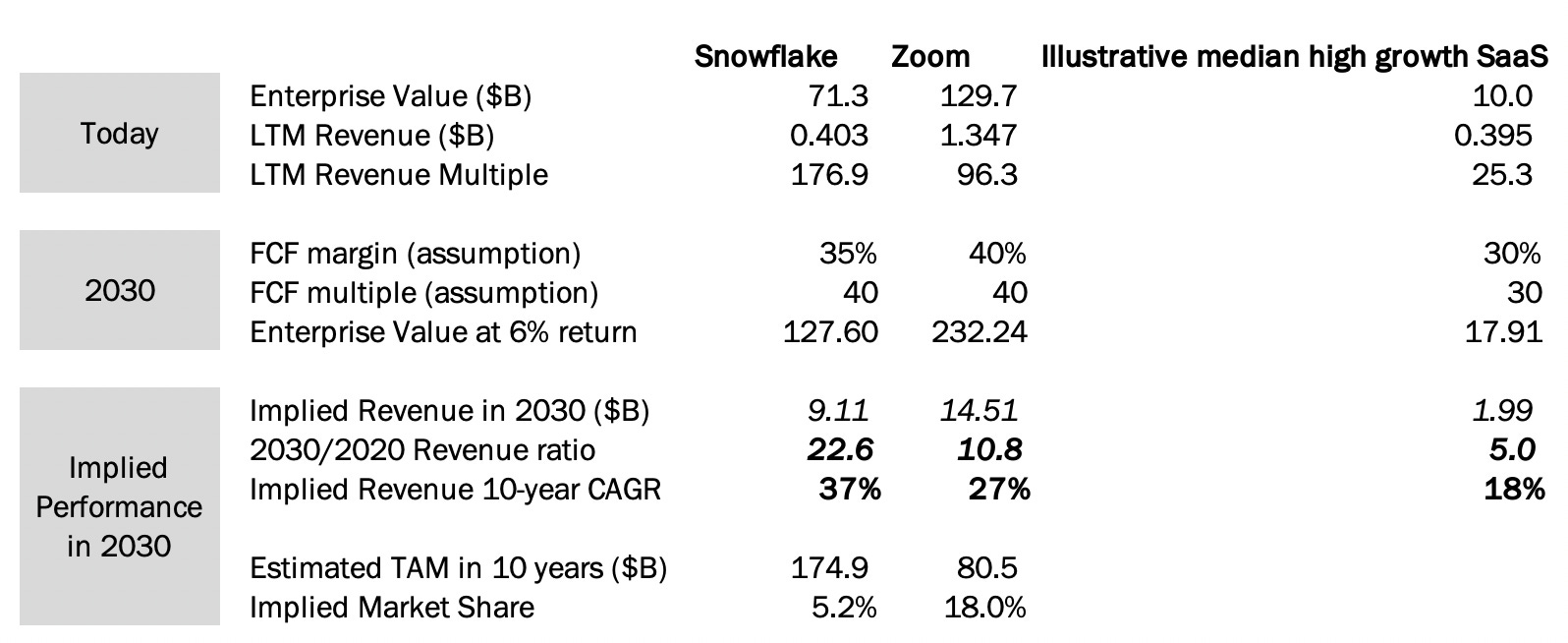

To illustrate what I’m talking about, we can look at Snowflake and Zoom, two companies which have some of the highest revenue multiples today.

By making assumptions on their long term FCF margin and their FCF multiple 10 years out, and assuming we want at least a 6% return between now and then, we can estimate that they need to grow their revenues by 23X and 11X respectively between now and then which is no easy feat. That’s a CAGR of 37% and 27% between 2020 and 2030. Given that they both had triple digit growth rates in the past year, that might not sound crazy, but we are talking about executing consistently over the decade to justify that valuation and earn a return.

We can also calculate how much market share they would need in 2030 of their TAM, which can be another data point, but not one I like a lot since TAMs change as markets change and companies enter new markets.

We can repeat the same exercise for the median high growth SaaS company which is today growing at 40% and has a ~25X multiple. 10 years from now, such a company needs to 5X its revenue, implying an 18% CAGR between now and then. While not crazy, that’s an impressive growth rate to achieve every year over the next decade, just to give investors a 6% return.

As an investor, the best way to use this is to assess what the market believes about a stock, and then see how your own expectations line up, to make a decision on whether to buy or hold a stock.

Overall, the multiples are high, but given the low interest rates and the growth of these companies, as evident from some of the numbers above, there is a clear path to justifying these valuations, although they do involve growing consistently over the next decade, and then generating FCFs of 30-35% of revenue.

so far i have been using p/s as a thumb rule for young growing tech companies. low p/s and high growth are key factors. p/s vs ev/fcf multiple differs. please write an article with examples on how growth affects multiples and how to think of high growth companies for say 5 years of future growth based valuations. thanks for the excellent insights.