Private Labels and Antitrust

Hi friends!

Last week, a bill titled Ending Platform Monopolies Act, among other bills geared at big tech, was proposed by Congress with bipartisan support.

This bill aims to reduce the conflict that may arise from a dominant online platform’s concurrent ownership of an online platform and other businesses.

While the bill has several components, one of them is that it would make it unlawful for a covered online platform to own a business that “utilizes the covered platform for the sale or provision of products or services”.

One of the immediate implications of this bill were it to be passed, is that it would require Amazon to split off or stop its private-label business. In some ways, the bill almost specifically targets this business.

I think it is a very strange bill for many reasons, which is what I will go into today.

Private Label Brands aren’t new

Amazon uses aggregated data about what products are doing well across the products it sells itself or sold via 3rd party merchants on its platform. And, if it sees an opportunity, creates its own brand to offer the same product, typically at a lower price.

This idea that a retailer uses aggregated data about what brands/products are being bought and decides to offer its own brand of products to compete with those products is, like many ideas in retail, not new. As Benedict Evans points out, “private label really goes back to department stores in the mid-19th century”. Sears was selling their own cameras along with those of other brands in the 1900s.

So this isn’t an area where tech has introduced something new which antitrust law of today isn’t fit for unless we believe that private labels in an online world are fundamentally different. More on that shortly.

Private Label Brands are a much smaller deal for Amazon

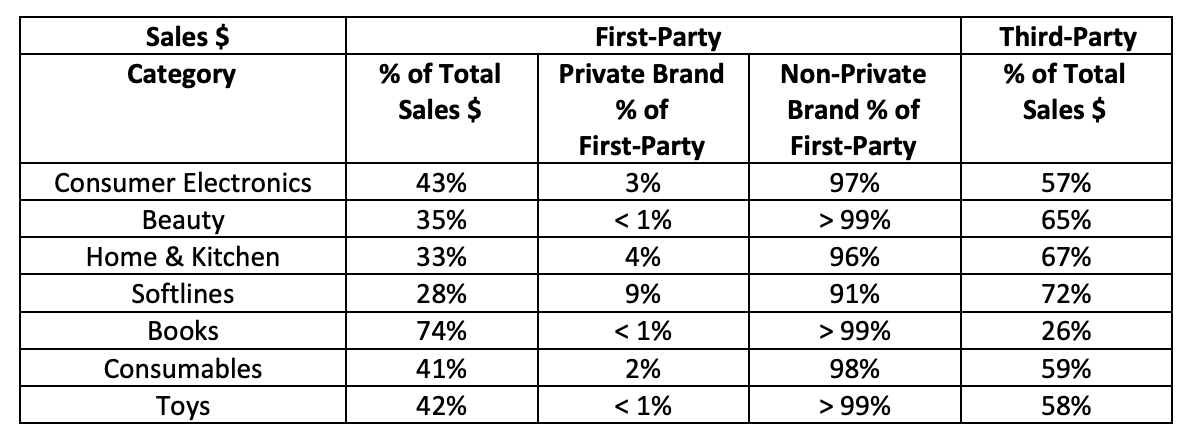

Bezos shed light on Amazon’s private-label business as part of a recent Antitrust proceeding, presented below.

As you can see, about ~40% of sales are first-party on average, and of those ~3-5% are from Amazon’s private label.

So, in aggregate, ~1% ($5-7B in sales) of the $500B in total GMV that Amazon does is from the private brand products.

How does this compare against other retailers?

Based on the chart below, the average across different types of retailers tends to be in the 20% region.

Amazon has the lowest share of private label sales by far!

So, a change in the law that requires splitting off or shutting down the private label business will affect these retailers a lot more than Amazon, right? Not quite.

The Bill basically only applies to Amazon

In the context of private label brands, the bill only applies to “covered online platforms”. And which online platforms are covered?

Platforms that have either:

More than $600B in revenue or market cap

More than 50M monthly active US users

More than 100,000 US monthly active businesses

So basically only Amazon. And that even though Walmart makes more revenue than Amazon, and multiple retailers do more in private label brand sales than Amazon.

There seems to be no good rationale for this choice of coverage other than to essentially carve out Amazon.

I understand the use of revenue/user/seller limits, but why market cap? And why is it set at the specific numbers it is set at? Why not $500B or $1T? (because Walmart would qualify if it were at $500B?)

What happens if a “platform” companies stock appreciates 20%? All of a sudden they shed their private label business?

Is there anything special about online?

One might argue that there’s something special about online platforms in this case and so the bill should only apply to Amazon.

But is anything really new about online in this context? Here are some of the typical criticisms:

Amazon uses data around product sales of what is selling on its platform to decide what products to develop: Offline retailers do the same. The key is that the data used is aggregated data.1

Amazon can place its products anywhere it chooses on the virtual shelf: Offline retailers can do the same. In fact, they typically place their private label brands right next to the recognized name brands and in more prominent places.

Amazon can make its platform pay-to-play by requiring sellers to pay to reach audiences: This exists in offline retail as well and is typically known as slotting fees. In addition, sellers don’t have to pay on Amazon to advertise. Many can get sales without advertising, and the take rates they pay on sales are comparable to what one might pay on rent/fulfillment, etc offline. In addition, Amazon allows a lot more sellers to easily reach audiences than the offline retailers do, which are much harder to get into.

Another thing to consider is what Bezos has pointed out before, that basically, third-party sellers are eating Amazon’s lunch, as Bezos’ quote below points out.

Over the past 20 years, third-party sellers have grown from 3% of sales of physical products by value in our store, to nearly 60%. Conversely, private brands sales represent only about 1% of our total sales.

They’ve grown to account for over half of sales, and that number is only going up. The master plan for Amazon has never been to move to more first-party sales, it’s always been the opposite.

Consumers like Private Label Brands

To add to all of this, in general, consumers like private label brands. They provide more choice and increase competition and tend to have lower prices.

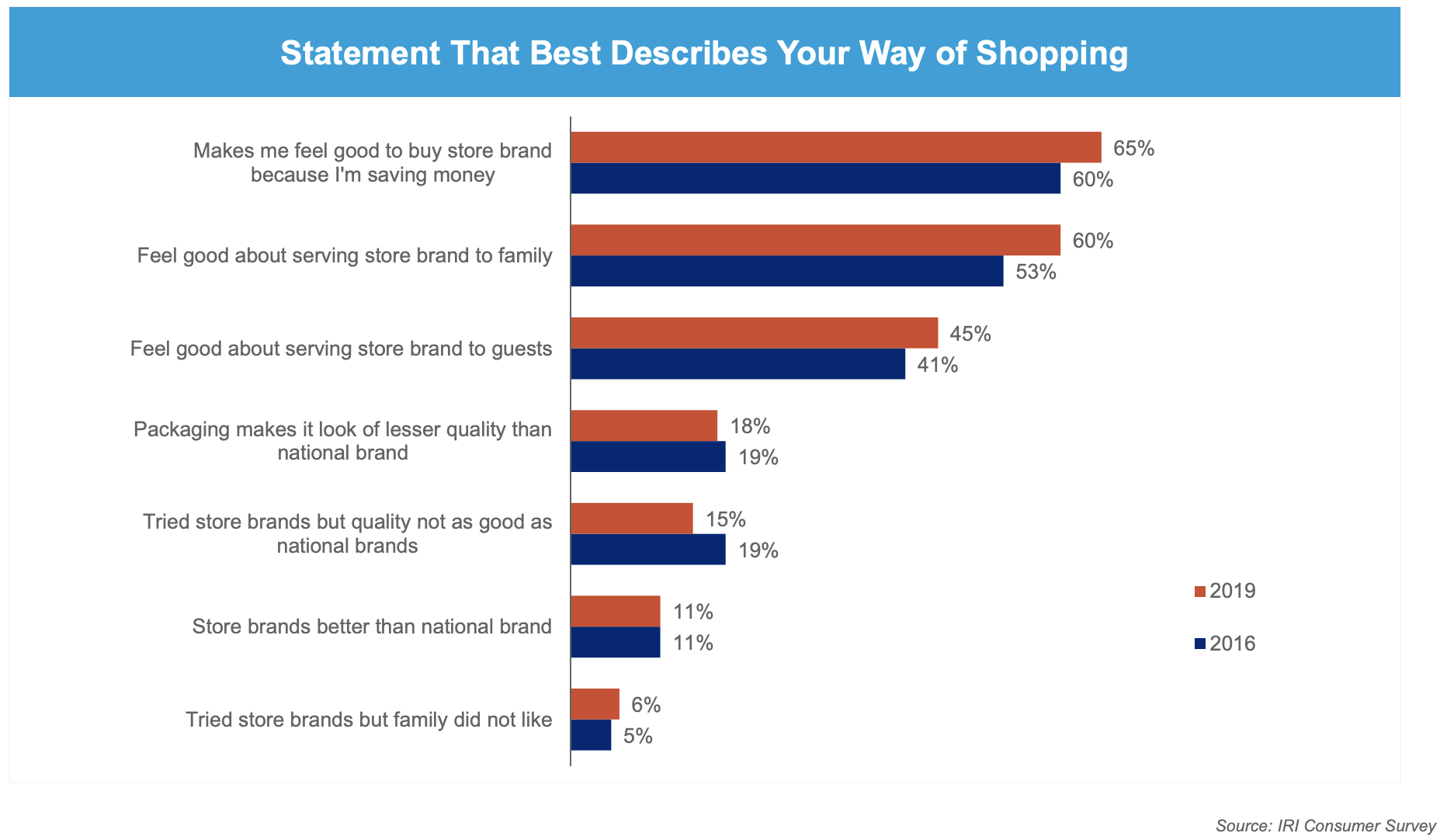

In a 2019 PLMA survey, two-thirds of consumers agreed with the statement, “In general, store brand products I have bought are just as good, if not better than the national version of the same products.”

In addition, 65% of consumers said that buying store brands made them feel good because it saved them money.

So from the typical consumer welfare barometer of antitrust, this bill is unlikely to accomplish anything good for consumers.

Closing Thoughts

If Amazon had to sell/stop its private label business, it probably wouldn’t make that much of a deal. For context, they make ~$5B in revenue from their private label brand, whereas they do >$20B in higher-margin advertising revenue on the third-party marketplace. They could probably substitute their private listings with ad slots on these searches, and make at least as much in margin would be my guess.

If it affects their entire first-party operation, that would be a bigger deal, since that’s ~40% of all sales, but presumably they would divest that or spin it out into a separate entity.

But the bigger question is, what is the point of the regulation? Are we against private labels in general? Or only in the online world? And is that because we’ve seen something happen online? Or do we want to just get ahead of it? If so, why only restrict the large companies? Why not stop any company from using this as a way to get large?

There is the possibility that certain employees at Amazon used non anonymized or aggregated information that went against their policies, which obviously should be investigated, but that doesn’t require Antitrust.

I'm trying to understand the rationale behind this bill too, and could only think of one counter-position.

I think it might come down to aggregated unit costs and target customers.

Its possible that Amazon's private label is primarily used by customers for low-cost items comprising lower expected quality and primarily non-perishables/non-consumables (for ex. cellphone chargers that are lost every 3 months). There's typically a lower opportunity cost to alternatives, thereby bullying out competition from SMBs who can't capitalize through quality.

If you compare that to Target's Room Essentials brand, for instance, the private label almost targets (pun intended) a certain audience that has lower purchasing power and quality expectation - college students. However, Room Essentials wouldn't monopolize over vendors and SMBs because of the existence of a wider market reach that involves consumers holding higher purchasing power and hunting for quality and uniqueness.

Would be interesting to see more refined data on the categories of items sold by various private labels compared with unit costs and perhaps volume.