IPOs in 2020 and the IPO Pop

The recent IPOs of Agora, Vroom, ZoomInfo, which all saw huge increases relative to their IPO price on the first day of trading (i.e., an IPO pop), got me curious about what the data for the year shows regarding IPO pops, which I dig into below.

The IPO Process at a Glance

Companies choose to go public for a combination of reasons, including

raising capital (though arguably a less important one for many companies with a plethora of capital available in private markets)

liquidity for earlier stages investors and early employees/founders

gaining more credibility with potential future employees or customers

instituting discipline throughout the organization

When a company wants to go public, the (highly simplified) process looks something like this: The company hires bankers who serve as an intermediary to help take it public. The bankers help craft the prospectus for the company which narrates the company’s story and serves a way to inform the public about the prospects of the company and includes an initial pricing range for the stock and an initial volume of stock the company intends to sell / money it plans to raise in the offering.

The bankers then run a marketing process known as the roadshow, where they pitch institutional investors on the company and its prospects and why they should invest in the company as part of its IPO. During this process, they are typically getting a sense of demand from investors, as well as the price they would be willing to pay. When all this is said and done, bankers will typically work with the company to update the number of shares offered and the listing price.

The IPO Pop and 2020 Data

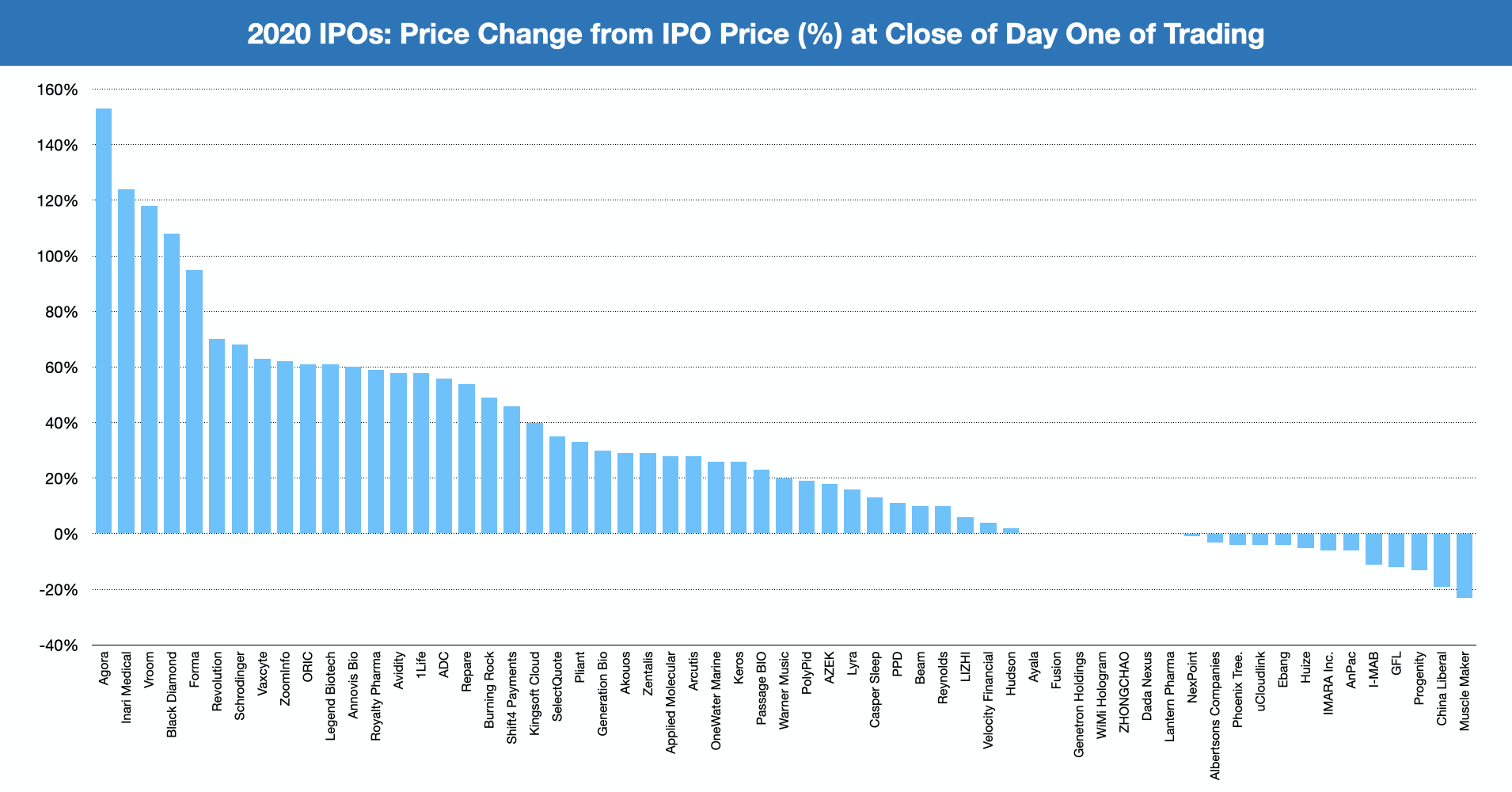

So how do banks do on pricing? Typically, IPO’s tend to “pop” on the first day of trading, meaning that they are underpriced relative to what the market was willing to pay. The data for 2020 helps support this.

Of 61 IPOs in the US in 2020, the median company that went public had a “pop” of 20% on the first day.

Only 25% of companies ended the day trading lower than their IPO price. Meanwhile, over 25% of companies ended the day, trading more than 50% higher than their IPO price.

If you had bought $1000 worth of each of the 61 companies at their IPO price (assuming you had access to that of course), your $61,000 investment would be up 29% after just one day of trading in each of the IPOs.

So what about the company going public?

If the companies that went public were priced perfectly, it would end the day within a few percentage points of the IPO price. If the closing price was a lot higher, then the company was diluted more than it should have been or raised less money than it could have otherwise, since it sold shares to investors in the IPO at less than what the market valued the shares.

Say a company sold 5M shares to institutional investors at $20 per share, raising $100M in its IPO and then ended the day trading at $30 per share (seeing a 50% pop). It ended up “losing” $50M, which is the additional money it would have gotten had the IPO been priced at $30.

In aggregate, the 61 companies that went public in 2020 so far raised $6.7B less than they would have been able to if their IPOs been priced at what the market valued the company. An IPO in 2020 shortchanged a company of $44M (median) or $110M on average, with some companies like Royalty Pharma, ZoomInfo, Vroom, and Agora especially losing out.

Why does this happen?

So why do banks tend to underprice IPOs? I think it mainly comes down to interests and incentives.

Note that the three key parties involved are the company going public, the bankers, and the institutional investors.

What does each of them want?

The institutional investors want to make a return on their investment, so their goal is to get the stock as cheaply as possible.

The bankers have to please both the company and the institutional investors and so have a delicate balancing act if the two sides’ interests differ.

But what does the company care about? On the one hand, it wants to raise as much money as possible while minimizing dilution. But on the other hand, it cares overall about the long-term success of the company (i.e., also the long-term stock price).

Now given these set of interests, here are three reasons I believe why IPOs tend to pop:

Banks take many companies public and often go to the same institutional investors again and again. Meanwhile, a company usually only goes public once. Therefore, while banks and institutional investors play this game repeatedly, most companies only play it once. With banks having to appease both sides, it’s not crazy to think they choose to satisfy the party they have a long-term repeated relationship with.

In addition, as mentioned above, companies themselves have interests that are at odds with each other. Given these interests, underpricing an IPO may indeed be the better move for them in the long-term if it leads to satisfied investors who continue to hold the stock and buy into the company story, and the company gets some of the momentum benefits of a strong IPO. Or at least that is what banks will try to convince the companies. Also, it’s important to note that while a company issues 15-20% new shares in the IPO, the rest is owned by founders/employees/ existing company investors. So all things equal, a company would rather start trading at a lower price and rise higher (your remaining 80% of shares appreciated) than start very high and drop to below what they might have been with a lower opening price.

Lastly, I think the media plays a role in this, as well. An IPO with a big pop is seen as successful in the media, whereas one without one is seen as unsuccessful (although in reality, the company got a better deal in the latter case). This increases some of the momentum and reputational benefits that a company might get from underpricing an IPO and provides further ammunition to banks to sell companies on underpricing (“Hey, you saw what happened to Facebook right? Let’s not be greedy with the IPO price…”)

So is there a better way? Some companies such as Slack and Spotify have used direct listings, which allow you to go public but today don’t allow you to raise primary capital, although that might soon change. I’ll touch on direct listings in the future, but if you’re curious to learn more about it, this Bill Gurley podcast goes into the topic in depth.

How many of you waiting for Snowflakes Ipo?