Customer-Based Valuation

Customer-Based Valuation

Linking customer lifetime value to company value

Hi friends!

With the growth of subscription (streaming, publications, enterprise software) and user-based transaction (eCommerce) or advertising (social media) oriented businesses, the usage and understanding of customer lifetime value and customer acquisition cost is becoming more commonplace.

They tend to be used internally in the company to make capital allocation decisions (marketing) and externally to make financing decisions (should we invest in the business based on the unit economics?).

However, one aspect that is still relatively underutilized internally and externally is taking a customer-driven approach to value creation and valuation, which I’ll cover in this piece.

This piece was partially inspired by the number of DMs I got with questions in response to this tweet, and the recent Mauboussin essay on this topic, which I highly recommend (along with the other resources below), which goes into this in more detail.

In the past, I’ve also written about how the income statements of some businesses don’t reflect true profitability because of intangible assets and investments in growing the user base where there is an initial cost upfront but the benefit occurs over time, which ties in well with this post.

I. What is customer-based valuation

Customer-based valuation refers to the use of customers as the atomic unit of analysis to estimate the valuation of a company.

Just like a DCF or other form of valuation analysis, the goal is to estimate the present values of the free cash flows of the business and therefore the valuation.

The difference is that the approach taken here is to determine the value at a customer or user level, and then scale that up to the number of customers to determine the overall value of a business.

It provides a direct bridge between the often-used concept of customer LTV to company valuation and is particularly useful for companies that tend to think about their performance in terms of users and user cohorts.

At a high level, it involves two parts:

Calculating the present value of a current customer is and multiplying it by the number of current customers

Calculating the present value of a future customer is (net of costs to acquire the customer) and multiplying it by the number of future customers

II. What businesses does this work well for

A customer or user-based approach to valuation works well for businesses where there is some level of recurring or re-occurring revenue at a user level. Typically, businesses that measure the number of customers or users they have and consider that as a strategic resource or asset can be valued well using this approach. Some specific industries this works well in are:

SaaS including SMB and enterprise for both subscription and usage-based models (Slack, Snowflake, Shopify, etc)

eCommerce and on-demand services including ride-sharing, delivery, convenience (Amazon, FIGS, Doordash, Uber, Lyft, etc)

Streaming and publication services including music, video, and other forms of media (Netflix, Spotify, NYTimes, etc)

Telcos including internet and cable (AT&T, Verizon, etc)

More generally, most subscription and transaction-oriented businesses, especially those which occur through digital channels such that users can be cleanly measured are good candidates for analysis at the customer level.

It could also be used for brick and mortar type businesses (e.g., restaurants or retail, etc), but typically a store-based approach works better there.

III. Basic methodology

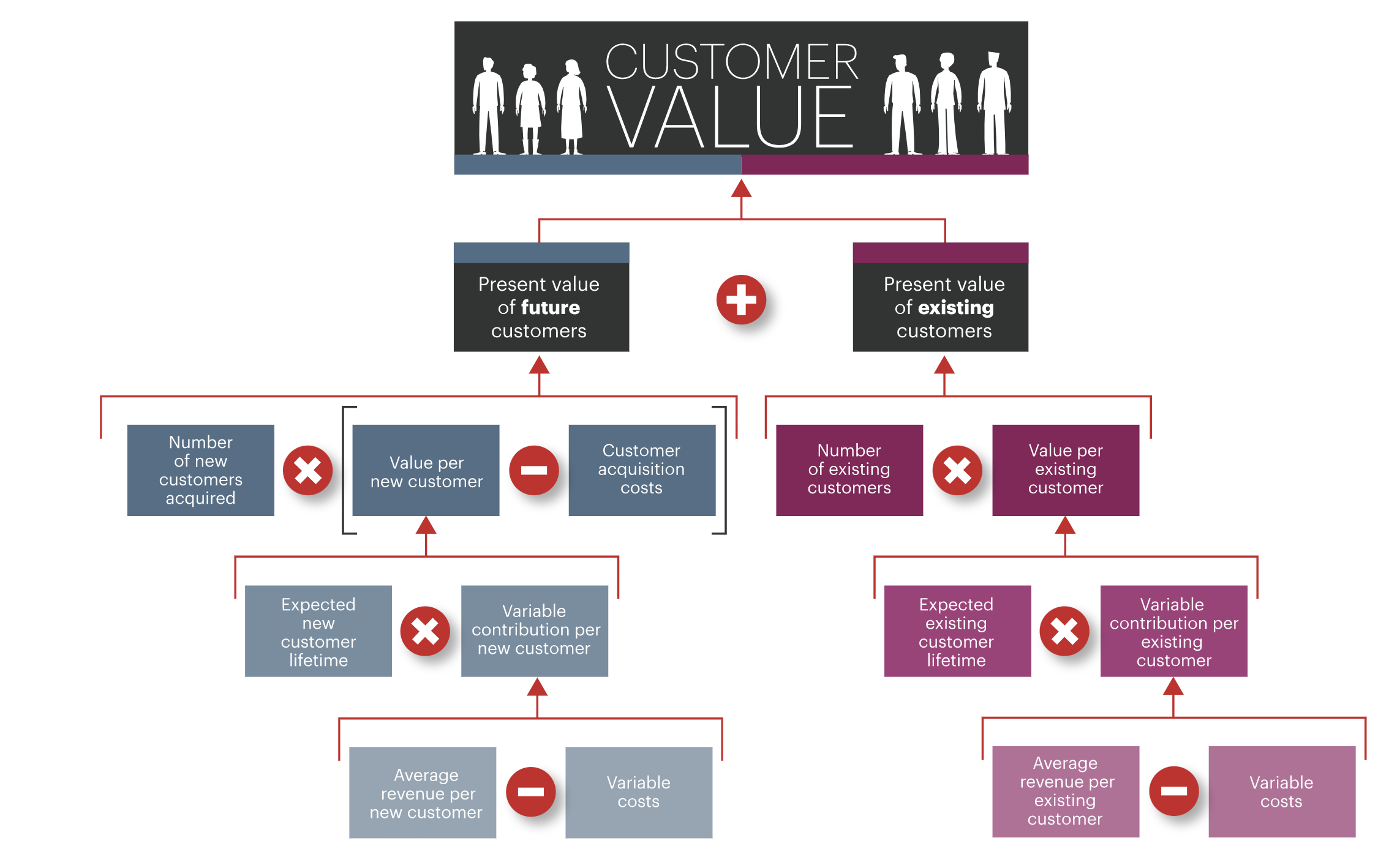

The typical approach is to estimate the present value of the current customer base and the present value of the future customer base.

At a high level, it can be thought of as LTV of existing user x number of existing users + (LTV of a new user - CAC to acquire new user) x number of new users.

The methodology is visualized below.

A few things to note:

When calculating the value of a customer, all costs should be considered, rather than just COGS which is sometimes used by marketing teams when calculating LTV. In addition, the value of future cash flows from a customer should be discounted back.

To estimate CAC for new customers, the easiest way typically is to consider marketing and sales spend in a period (spent on acquisition and not retention) / the number of customers added in that period. Typically, assuming some increase in CAC over time is prudent.

The number of new customers acquired should be based on the TAM and assume a realistic share of TAM given the market structure and competitive dynamics, and take into account the increasing CAC as a company further penetrates the market.

The value of a customer tends to be very sensitive to churn (existing customer lifetime is just 1/churn) and so companies should be conservative when estimating churn.

IV. Tying customer-based valuation to value creation

The methodology above clearly visualizes what the key elements to value creation are, which I detail below. These should be fairly familiar to those who’ve seen the equation for lifetime value before.

Increasing value from the existing customer base

Increase revenue per customer by cross-selling / upselling or adding features to increasing usage volume/transaction volume

Reduce costs to serve existing customers by reducing gross margins, marketing spend on customer retention, R&D/G&A per customer, etc

Reducing churn through additional product features or better sales and customer support

Increasing the number of existing customers by acquiring new customers.

Increase value from the future customer base

Reduce customer acquisition cost by improving marketing or sales efficiency or implementing referral programs, partnerships other distribution approaches

Increase future customer lifetime value through any of the means mentioned above as well as better user onboarding and other product improvements which increase the rate of customer adoption / reduce new user churn

Increase the estimated size of the future customer base by growing the TAM or the penetrable TAM by layering on products and adding on product features and entering into adjacent markets and improving the overall GTM approach and solution

What I like about the above, is that it clearly shows how improvements across any function can increase the value of the company and what the key levers are. It is often a lot easier to see how a specific team in the company, whether it be a sales or product team or customer support or ops team is creating value for the company by considering which of these drivers they are moving.

V. Benefits of customer-based valuation

You might be wondering if there are any other benefits other than the cleaner value creation drivers I highlighted. Let’s go into them from an internal perspective and an external perspective.

Internal

Using a customer-based valuation approach internally either for capital allocation of prioritization (whether directly) or through a focus on driving LTV and reducing CAC can be helpful for a company in the following ways:

Makes it easier for employees to see how their work creates value for the company and drives the companies valuation

Makes it easier for management teams to prioritize different initiatives within and across functions based on value creation

Allows for a long-term orientation by highlighting things that may reduce accounting profits in the short term but increase valuation and making it easier to allocate capital to them. As an example, when CAC is lower than LTV and the payback period is longer than a quarter, spend on marketing to acquire customers will reduce earnings that quarter but increase the value of the firm. This lens to capital allocation reduces short-term positive but long-term suboptimal decisions.

External

For outside investors and analysts, a customer-based valuation approach can be a better way (or another way to complement existing ways) to gauge the performance of a firm and understand its true earnings potential, in the following ways:

The more bottoms-up nature of forecasting through customer-based valuations allows for models which better capture the realities of a business such as increasing CAC as penetration goes up as well as the improving economics or increasing usage of cohorts as the mature / graduate.

Customer-based valuation allows for tracking and measuring the performance of a business on a quarterly or an annual basis in a way that isn’t captured in the typical accounting statements. Companies that are unprofitable in an accounting sense but are actually investing heavily in customer growth and have profitable unit economics may be more intrinsically valuable quarter over quarter which may not get captured in either the topline revenue growth (lots of new customers who take time to mature) or earnings (one-time marketing expenses while the revenues from those customers come over time)

When used in a reverse-DCF type way to estimate what expectations are implied given market valuations, it can be used to gauge what the market expects from a business in terms of customer growth and penetration and to understand what share of a business valuation comes from existing users vs future users.

VI. Pitfalls

While customer-based valuation is a useful technique to estimate the value of certain types of businesses, one needs to be careful in the assumptions and estimates they make and keep in mind the following.

After all, just like DCFs or any other models, you can kind of get them to say what you want them to say.

Customer lifetime values are dynamic: They are estimates applicable to a moment in time, and not completely precise.

CACs tend to increase: While companies tend to decrease CAC as they figure out their marketing and sales playbook initially, beyond a point CACs tend to go up over time as market share goes up.

The future customers need not be worth the same as current customers. All things being equal, the new marginal customer probably has a lower LTV (ignoring product improvements, etc) given that they were a relative laggard. On the flip side, in companies that say move upmarket, the opposite might be true.

Value comes from current and future customers: I often see takes like, “Clubhouse has 5M users and is worth $4B, that means each user is being valued at $800. What a joke!!” As another example, graphs like below which compare valuation per subscriber/user are common. What this misses is that different companies are at different points in their growth trajectory and so maybe at 1% of their potential user base or 95% of their potential user base (and of course they might monetize these users differently). So using valuation and considering only current subscribers, especially for more nascent companies is pretty disingenuous.

Closing Thoughts

Customer-based valuation is a good approach to consider for valuing businesses where a customer base or user base is a key strategic resource and where there is a transactional, usage, or subscription-based element to customer use and revenue.

It can be a more straightforward lens to understand value creation within a company and to easier model the performance of a company where users or customers are the atomic units of value creation.

If you ever see a deck or filing with a customer cohort chart like the ones below, a customer-based analysis approach would work well to understand the business.

Resources

Here are a few resources for those interested in reading more about this topic.

I may also go through an in-depth example in a future post if there’s interest.

Peter Fader and Daniel McCarthy’s How To Value a Company by Analyzing Its Customers

Dan Callahan and Michael Mauboussin’s The Economics of Customer Businesses

Thanks for reading! If you liked this post, give it a heart up above to help others find it or share it with your friends.

If you have any comments or thoughts, feel free to tweet at me.

If you’re not a subscriber, you can subscribe below. I write about things related to technology and business once a week on Mondays.

Great read!

How do you discount the customer value? What is the most appropriate discount rate and what is the time horizon over which the discounting would be done?

Since the future customer value would be spread across a long period for different kind of startups, how to arrive at the most appropriate time period?

Tanay, nice work.

I think you have done a good job of outlining customer-based valuation.

A couple of suggestions of things that I would consider a little differently.

Firstly, the Bain graphic seems confusing to me -- discounting clearly happens somewhere to get to 'present value' but I would much prefer it to be explicit. (This is probably less of a concern for finance/marketing people but plenty of marketers forget to discount -- I'd like to be more upfront in discouraging that).

More substantially the argument that "all costs should be considered" makes sense for external analysis but not for the internal analysis that you recommend. I am reminded of the confusion in Selden and Covin's Angel Customers and Demon Customers (https://www.amazon.com/Angel-Customers-Demon-Discover-Turbo-Charge/dp/1591840074/). Full costs allocation is a major challenge for internal decision-making.

Finally, I'd move "Increasing the number of existing customers by acquiring new customers." I don't think this is, by definition, should come under "Increasing value from the existing customer base" given it is not related to the existing customers.

Still nice work on a clear summary.

Neil Bendle, Associate Professor, University of Georgia, https://neilbendle.com/